Advance Analytics:

Leveraging Advanced Analytics to Drive Customer Behavior in the Airline Industry.

The past decade has been tough for airlines, due to a wide array of macro-economic factors, socio-political uncertainties, increased cost of operations, a stagnating and in some cases even declining market and tremendous increase in competition. In light of these challenges, airlines need to continuously reinvent themselves and stay connected with customers, increase returns on every dollar spent and build a loyal customer base.

Advanced analytics can be leveraged by airlines to address these challenges by improving their customer centricity. It looks at customer behavior in the airlines industry from three aspects. We start with the hypothesis that any numeric customer index that captures the value of the customer to the airline needs to reflect the heterogeneity of customer behavior. This can be best achieved by using a multi-dimensional customer index, or what we call the Customer Composite Vector (CCV).

Secondly, a numeric customer index (single aggregated score or multi-dimensional vector) is not only a way of understanding customer behavior, but it also has the potential to be used by airlines as a lever to shape and drive customer behavior in a manner that increases customer yield and profitability.

Last, but not least, looking at the customer through the lens of CCV will allow airlines to treat customers differently by leveraging their heterogeneity and allowing for connections at an individual level. This, we believe, will increase customer loyalty and overall brand equity over time. We also offer a vision of the technology infra-structure required to make CCV a reality, including custom in-house deployments or delivered as hosted, managed application services.

Satisfying customer demand is not sufficient; airlines need to shape and drive existing customer behavior in a manner that maximizes returns and keeps them one step ahead of both the customer and the competition.

Advanced analytics can enable airlines to gain an increased understanding of customer behavior patterns, identify a cost-optimized way to serve them, enhance opportunities for revenue generation and build strong brand perception/loyalty among existing and potential customers.

This and more can be accom¬plished by leveraging proven statistical and scientific methods. These methods can significantly improve the quality of decisions by reduc¬ing “gut-feel” decision-mak¬ing and increasing scenario-based decision-making that is fortified with data-derived foresight. In today’s hyper-competitive marketplace, advanced analytics can be the crucial element in identifying ways for airlines to differentiate themselves with customers and ensure continu¬ous business improvement on an ongoing basis.

Creating a single customer score is valuable; however, it also has its limitations, as the heterogeneity of customer behavior is lost when it is aggregated under a single score.

Airlines are obsessed with new customer acqui¬sition. However, they also realize the importance of retaining and generating more revenue from existing customers while enriching their experience and thereby increasing cus¬tomer loyalty and stickiness. They have worked hard to understand customer behav¬ior, with varying degrees of success. The key question is how airlines can move beyond merely understanding custom¬er behavior. Our fundamental hypothesis is that satisfying customer demand is not suf¬ficient; rather, airlines need to shape and drive existing customer behavior in a manner that maximizes returns and keeps them one step ahead of both the customer and the competition.

Limits of Traditional Customer Scoring: At most airlines, customer data is generated by different sources and is manifested in different shapes and sizes. Some examples include ticketing data (e.g., owned and online travel agency Web sites, intermediaries, agents, etc.), frequent flyer data (e.g., owned, alliance or third-party), marketing data (e.g., partner information) and callcenter data. Many have attempted in several ways to understand the profitability (i.e., cost-to-serve) or to link non-travel revenue with other customer data; however, they have not found any direct mechanism to compute it.

In an attempt to use disparate customer infor¬mation, they end up creating multiple versions of customer databases, each specific for each requirement. In some cases, airlines have hundreds of different customer databases, each built for analyzing customer data in a different way. While many airlines have consolidated customer data from disparate sources under a common customer database or data warehouse, they have not yet been very successful in utilizing the insights this data reveals in a cohesive manner.

Most airlines currently have one view of the customer through their customer loyalty database, and they use frequent flyer data to differentiate customer profiles — which may not be an accurate reflection of their lifetime value or profit contribution. Some have even gone a step further and used customer data to assign a score to customers, indicating the relative value or importance of individual customers. Creating a single customer score is valuable; however, it also has its limitations, as the heterogeneity of customer behavior is lost when it is aggregated under a single score.

Sometimes, customer scores are used to quantify the value of the customer from a lifetime per¬spective. Such a value does not provide insight into the customer’s behavior at any particular time, and it does not provide any insight on how to change the customer’s current behavior to the airline’s advantage. A single customer score or lifetime value does not provide any indication of how airlines can connect better with the customer, ultimately resulting in increased yield and spend. More specifically, it does not help airlines to assess how different offers may have a different impact on different customers.

Customer Composite Vector: A Multi-Dimensional Customer View An alternative to an aggregated customer score is a Customer Composite Vector, or CCV, which can form the foundation for generating customer-specific actionable insights. By definition, CCV is a multi-dimensional customer value along a set of ehavioral dimensions or vectors. The definition of vectors will differ from industry to industry.

For AirLines

Future of Airlines: Substitution and Commoditization

Now is the time for airlines to take the lead in developing and introducing seamless travel solutions that enable customers to see air service for what it is: one of many steps in a complex dance that, properly orchestrated, can become enjoyable once again.

After looking at impact of oil prices to Airline Carriers that hope the worst is over with regard to oil price spikes might remember harboring the same hopes in 2008 when oil was at US$105 per barrel. So what can carriers that suspect this is the beginning of another swing in the wrong direction do? As outlined in our report, “Future of Airlines Substitution and commoditization,” we believe the best course involves carriers finding low-cost ways to differentiate themselves by delivering improved customer experiences and reinventing their marketing models.

Cost cutting was essentially the only way out of the 2009 crisis – and some carriers have room to make further cuts today. However, those that have already made the big, the small, and even the most difficult tiny cuts should look at the other side of the profitability equation. In addition to focusing on revenue growth, carriers should seek to improve revenue quality through better marketing. Now is the time to reinvent products and services by abandoning those strategies aimed at the masses. Rather, carriers should target those customers to whom they can offer superior service – service surpassing that offered by any of their competitors. Marketing expenditures should go toward sharing these value-added features with customers and reminding them exactly why the airline is unique.

Price premiums and loyalty should be built around service components not offered by competitors, so an increase in marketing spend does not mean subsidizing another fare sale. Carriers should approach product reinvention with a realization that the product itself is not the problem. The service that surrounds and defines the airline product delivery is as much a commodity as the flat-bed seat and in-flight entertainment that is often included (for a price in many cases). Carriers should seek to give customers what they really want: a less stressful, more integrated journey.

Now is the time for airlines to take the lead in developing and introducing seamless travel solutions that enable customers to see air service for what it is: one of many steps in a complex dance that, properly orchestrated, can become enjoyable once again. Today’s passengers move from the relative sanctuary of their home or office through a crowded city, into harried airports, past stress-producing security lines and onto crowded planes. They then spend a few hours on a plane where they are provided physical products and in-flight services designed for everybody (and, therefore, nobody in particular). Finally, they are stuck in a crush of humanity fighting to retrieve luggage and find a taxi, bus, train or car to get them to their hotels and other destinations.

How might this experience change for passengers whose carriers heed the advice proffered in “Future of Airlines ” report? For starters, these customers could enjoy the benefits of a more streamlined shopping experience. Similar to the book, music and product suggestions shoppers get from leading web retailers, airline websites could more effectively leverage the sea of information available from each passenger to make targeted suggestions and more relevant offers. Rather than spending five hours shopping for a two-hour flight, travelers would receive suggestions based on their search context and tailored to their needs.

Additionally, carriers should offer customers not only the option of booking associated pieces of the travel process on the airline’s Web site, but also the option of tracking and managing the entire journey. Tactically, this involves carriers coordinating with other travel providers like hotels, ground service companies and even travel agents. The objective is to make the experience seamless for the traveler by offering choices on their handheld device or via phone that account for the full impact of a schedule change, different route or cancelation. Today, travelers have to manage these sorts of changes on their own, and many consumers are not well equipped to account for the complexity of an entire journey when they are in the middle of it.

Finally, looking a bit further into the future, airlines should view the next crisis (whatever form it takes) as an opportunity to do some long overdue reinvention. Some carriers have already started down this path. Those that haven’t need to realize that completely new approaches are required to successfully compete against incumbent airlines that have undergone reinvention or with high-speed rail providers offering new and compelling value propositions.

Bigger may not always be better, especially from the perspective of customers, so airlines should consider programs and changes based on more narrow segments, not on casting an even wider net. Products, services and even the airline brands should be more meaningful to the target consumers. And if sub-brands with their own unique service profiles (like global hotel chains) are the most efficient way to differentiate the customer experience, then they must be considered. Obviously, not all carriers will heed these suggestions. However, we believe those that do will not only weather brewing storms more effectively, they will also emerge from the next crisis with a more meaningful set of products and services, a more loyal and less price sensitive customer base, and a more favorable competitive position in what is sure to be a more competitive marketplace.

For AirLines

Mastering Information for Competitive Advantage: Smarter Computing in the Travel and Transportation Industry

Mastering Information for Competitive Advantage: Smarter Computing in the Travel and Transportation Industry

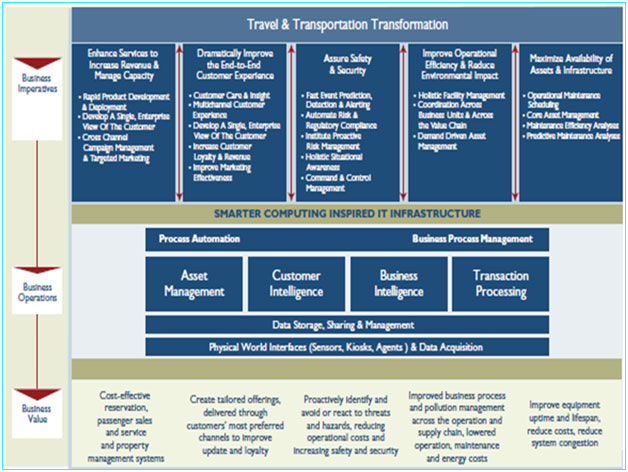

The travel and transportation industry remains a key component of the global economy. As the industry evolves and becomes more complex, the amount of information service providers need to handle is growing. Traditional information technology (IT) infrastructures often cannot cope with the volume and velocity of data generated across the industry, which leaves some companies at a competitive disadvantage. Smarter Computing is a new approach to help CIOs better design and implement business infrastructures to support new growth and deliver operational efficiency. By applying Smarter Computing principles, a number of service providers are becoming more effective, efficient and agile, and are realizing significant business value from transforming their IT infrastructures.

INFORMATION OVERLOAD FOR TRAVEL AND TRANSPORTATION PROVIDERS

“The proliferation of travel booking channels makes it ever more difficult to get a consolidated view of a seemingly simple question: How many people want to fly between A and B, and how much will they spend?”

Transportation is vital to maintaining our globalized society. Although business models based on distributed supply chains, outsourcing and partner eco-systems establish borderless interrelationships, it is the physical transportation of goods and people that truly enables globalization. Today’s travel and transportation systems are dependent on an efficient and intricate global network of air, rail, road and water links. The travel and transportation market overall is shifting from the predictable structure it traditionally enjoyed, as the volume of passengers and freight continues to grow and the competitive intensity in the market increases. Transportation systems are generating vast amounts of information. Managing and utilizing it are sources of significant challenge to travel and transportation service providers.

Travel and transportation service providers need to develop new methods and business models to compete as the industry changes. Traditional models are proving ineffective due to factors such as the lingering impacts of uneven economic expansion in mature and growth markets, the effects of natural disasters and security threats and the proliferation of sales channels. The amount of information that is relevant to businesses under these factors is increasing the complexity of creating and implementing business strategy. David Doctor, director of Distribution Marketing for Amadeus, highlights the issue. “The proliferation of travel booking channels makes it ever more difficult to get a consolidated view of a seemingly simple question: How many people want to fly between A and B, and how much will they spend?”1 Added to this, congestion and delay are ongoing issues for many transportation systems. Traditional solutions that involve building additional or upgrading existing transportation infrastructures are expensive, with one estimate suggesting 2.5 percent of global gross domestic product (GDP) would be needed annually to keep up with demand. 2 Travel and transportation service providers need to find ways to meet a growing demand with efficiency, consistency and profitability.

The transformation process itself is a challenge to travel and transportation providers because it implies the need to carefully organize and process large amounts of data in new ways. Much of this data is likely to reside in silos within and outside of the organization, which needs to be consolidated and shared where necessary and permitted, to achieve the imperatives. The legacy information technology (IT) infrastructures in the industry tend to be inflexible to accommodate business transformation and the variety of systems (some of them homegrown or even manual) that may be scattered throughout the industry ecosystem. By extension, the traditional IT architecture, featuring a single server or clusters of servers dedicated to one type of workload, contributes to complex and costly server sprawl. Other concerns about the downtime associated with outages or unplanned maintenance, peak traffic overwhelming processing capacity and the high levels of management needed on a large number of servers can create huge costs to providers.

The process of generating business value shown in Figure 2 illustrates that travel and transportation service providers can use a Smarter Computing-inspired IT infrastructure to deliver the outcomes inherent in the industry imperatives. The IT infrastructure enables new business processes and enhances the performance of existing operations to increase customer satisfaction and loyalty while controlling costs and pollution throughout the enterprise operations. Within each of the imperatives, an infrastructure that is designed for data, workload optimized and managed with cloud technologies can deliver real business value.